Corporate debt restructuring is a strategic financial arrangement in which a company facing liquidity challenges reorganizes its existing obligations. By renegotiating terms with creditors, businesses aim to mitigate the risk of bankruptcy or insolvency. This process is a vital tool for distressed companies that remain operationally viable but require a recalibrated capital structure often involving the modification of a business loan to manage financial pressure and restore long-term stability.

The restructuring process involves the professional negotiation of repayment terms, such as extending loan tenures, adjusting interest rates, or revising payment schedules. In certain complex cases, advisors may facilitate debt-for-equity swaps or a temporary moratorium on payments to restore immediate liquidity. These measures are implemented upon the formal approval of banks and financial institutions, designed to assist companies in meeting their long-term debt obligations sustainably.

Unlike mandatory court filings, corporate debt restructuring is often a voluntary process conducted outside the judicial system. When initiated early with expert advisory, it supports uninterrupted operations, protects creditor interests, and strengthens the company’s financial foundation.

Why Corporate Debt Restructuring Is Needed: Financial Distress vs Insolvency ?

Financial distress occurs when a company struggles with liquidity due to rising service costs or revenue fluctuations. Insolvency, however, is a legal state arising when liabilities exceed assets or obligations cannot be met under the bankruptcy code. Restructuring is most effective as a preemptive measure to avoid court-driven proceedings.

Common Warning Signs of Financial Stress

Companies should evaluate restructuring options when experiencing:

- Persistent cash flow shortages affecting daily operations.

- The occurrence of missed or delayed debt repayments.

- A rising interest burden that thins operating margins.

- An over-dependence on short-term credit for long-term needs.

- Strained working capital cycles.

Industries Where Debt Restructuring Is Most Common

Restructuring is a frequent strategic requirement in capital-intensive sectors such as:

- Manufacturing and industrial sectors.

- Infrastructure and construction.

- Real estate development.

- Aviation, logistics, and power projects. These industries often manage large-scale debt and are highly susceptible to economic volatility.

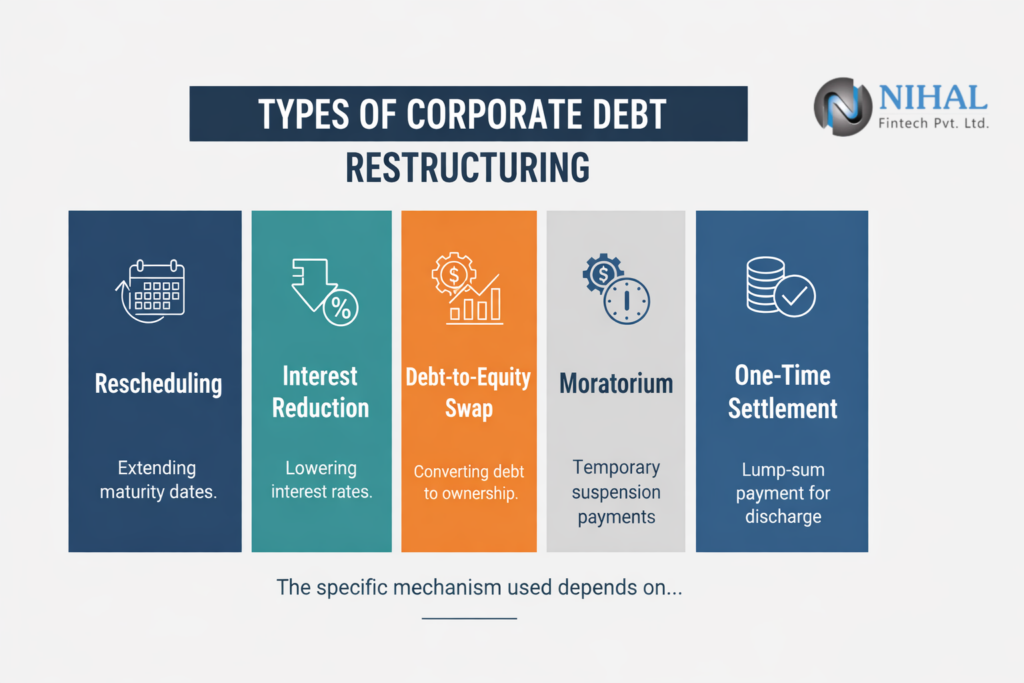

Types of Corporate Debt Restructuring

The specific mechanism used depends on a thorough lender assessment and the underlying viability of the business model.

Corporate Debt Restructuring vs Insolvency & Bankruptcy (Table Formate)

While restructuring focuses on business revival through negotiation, insolvency proceedings are governed by the Insolvency and Bankruptcy Code (IBC) and involve judicial oversight.

| Feature | Corporate Debt Restructuring (CDR) | Insolvency & Bankruptcy (IBC)Insolvency & Bankruptcy (IBC) |

|---|---|---|

| Nature of Process | Flexible, out-of-court negotiation. | Formal, judicial oversight (NCLT). |

| Legal Framework | Contractual agreement between debtor and lenders. | Governed by the Insolvency and Bankruptcy Code. |

| Management Control | Existing management retains control of the company. | Management is usually replaced; control shifts to the CoC and an IRP. |

| Flexibility | High; terms can be customized to specific needs. | Low; follows strict statutory timelines and procedures. |

| End Goal | Business revival and debt rescheduling. | Resolution of debt or liquidation if no plan is viable. |

| Stigma/Publicity | Usually private and carries less market stigma. | Public process that can impact brand reputation. |

Corporate Debt Restructuring vs Debt Refinancing

| Feature | Corporate Debt Restructuring | Debt Refinancing |

|---|---|---|

| Primary Goal | To prevent default or bankruptcy during financial distress. | To secure better terms (lower interest, longer tenure). |

| Company Health | Usually for companies facing liquidity stress or insolvency. | Usually for financially healthy or creditworthy companies. |

| Process | Renegotiating terms with existing creditors. | Replacing an old loan with a new loan (often from a new lender). |

| Control & Oversight | High lender oversight; management may face restrictions. | Standard commercial activity; management retains full control. |

| Credit Impact | Can negatively impact credit ratings due to “distress.” | Often improves credit profile if it lowers the debt burden. |

| Market Perception | Seen as a sign of financial trouble. | Seen as smart financial management. |

Legal Framework Governing Corporate Debt Restructuring

Restructuring in India is conducted under the stringent guidelines issued by the Reserve Bank of India (RBI) and involves a collaborative effort between banks, NBFCs, and specialized financial advisors.

Role of Lenders and Financial Institutions

Lenders are responsible for assessing the techno-economic viability of the proposal. They monitor compliance through established frameworks, ensuring the restructuring plan is fair and sustainable.

Relationship With Insolvency and Bankruptcy Code (IBC)

Restructuring serves as a critical, proactive alternative intended to resolve stress before the need for a formal Corporate Insolvency Resolution Process (CIRP).

Regulatory Considerations

All restructuring activities must ensure complete transparency, comply with RBI norms, and treat all classes of creditors fairly to remain legally sound.

Benefits of Corporate Debt Restructuring

- Avoidance of Bankruptcy Proceedings: Protects the brand’s reputation by resolving issues privately.

- Improved Cash Flow & Liquidity: Realigns debt obligations with actual income to restore balance.

- Business Continuity: Ensures that operations, vendor relationships, and jobs are protected.

- Preservation of Lender Relationships: Rebuilds trust through transparent and honest communication.

- Long-Term Financial Stability: Creates a sustainable capital structure for future growth.

Risks and Challenges of Corporate Debt Restructuring

- Potential impact on corporate credit ratings.

- Strict operational and financial monitoring by lenders.

- The necessity for rigorous financial discipline and reporting.

When Should a Company Consider Debt Restructuring?

Management should consider restructuring at the first sign of sustained financial stress. Early action dramatically increases the chances of a successful negotiation with lenders.

Real-World Example of Corporate Debt Restructuring

A manufacturing client facing high interest costs and a sluggish market may work with advisors to extend their loan tenure. By restructuring the debt to match their current cash flow, the firm avoids default and secures the liquidity needed to continue production.

Frequently Asked Questions

-

Is corporate debt restructuring the same as bankruptcy?

No, corporate debt restructuring is not the same as bankruptcy. Restructuring is a negotiated, out-of-court arrangement that allows the company to continue operating under existing management while working toward financial recovery. Bankruptcy, on the other hand, is a formal legal process that may result in court oversight, loss of management control, or even liquidation of the business. Restructuring is generally preferred when the business is still viable.

-

How does corporate debt restructuring help businesses?

Corporate debt restructuring helps businesses by reducing immediate financial pressure. Lower monthly repayments, reduced interest costs, or temporary payment relief improve cash flow and provide time to stabilize operations. This breathing space allows management to address underlying business challenges, improve performance, and rebuild long-term financial health without disrupting day-to-day operations.

-

What types of debt can be restructured?

Most corporate debts can be restructured, subject to lender approval. This typically includes term loans, working capital facilities, project finance loans, and in some cases unsecured borrowings. The scope of restructuring depends on the company’s financial condition, the nature of the debt, and the willingness of lenders to modify existing terms based on recovery prospects.

-

Does debt restructuring affect my credit score?

Yes, debt restructuring usually results in a credit rating adjustment because it signals financial stress. However, the impact is generally less severe than that caused by an outright default or insolvency proceedings. From a lender’s perspective, restructuring is often seen as a responsible effort to manage obligations and protect repayment capacity rather than a failure to honor debt commitments.

-

Who approves a corporate debt restructuring plan?

A corporate debt restructuring plan must be approved by the lenders involved, including banks, non-banking financial companies (NBFCs), and other financial institutions that provided the original loans. Approval is typically based on the company’s viability, projected cash flows, and the likelihood that restructuring will result in better recovery outcomes than legal enforcement or insolvency.

-

Can a company restructure debt more than once?

While it is possible for a company to restructure debt more than once, repeated restructuring can significantly reduce lender confidence. Multiple restructurings may indicate deeper financial or operational issues and can limit access to future financing. Lenders may impose stricter conditions or decline further support if restructuring attempts do not lead to sustained improvement.

Conclusion

Corporate debt restructuring is a powerful recovery tool and a sophisticated mechanism that allows distressed companies to reorganize their liabilities and rebuild stability. By choosing to restructure, companies can protect their future, maintain uninterrupted business operations, and rebuild financial health within the global ecosystem. When managed by expert advisors and initiated early, it serves as a powerful shield for the debt of companies facing financial hurdles.Secure Your Company’s Financial Future Don’t wait for financial stress to become insolvency. If your business is navigating complex corporate debts, our team at Nihal Fintech is here to help you renegotiate new terms and restore liquidity.

Contact Nihal Fintech today to discuss a bespoke restructuring plan and take the first step toward long-term financial stability.

Disclaimer: This article is for general informational purposes only and does not constitute financial or legal advice. Corporate debt restructuring is subject to lender approval, RBI guidelines, and applicable laws. Nihal Fintech does not guarantee approval or specific outcomes. Please consult a qualified financial or legal professional before making decisions.