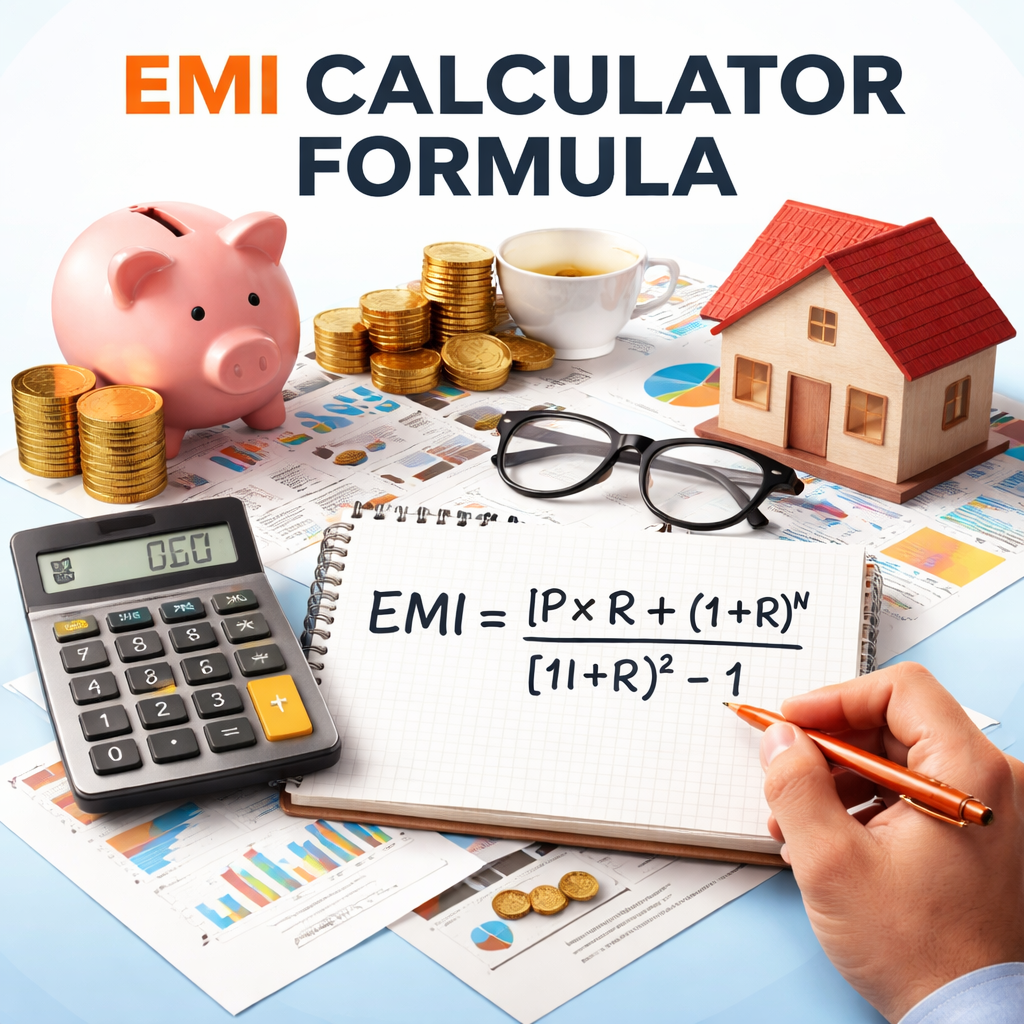

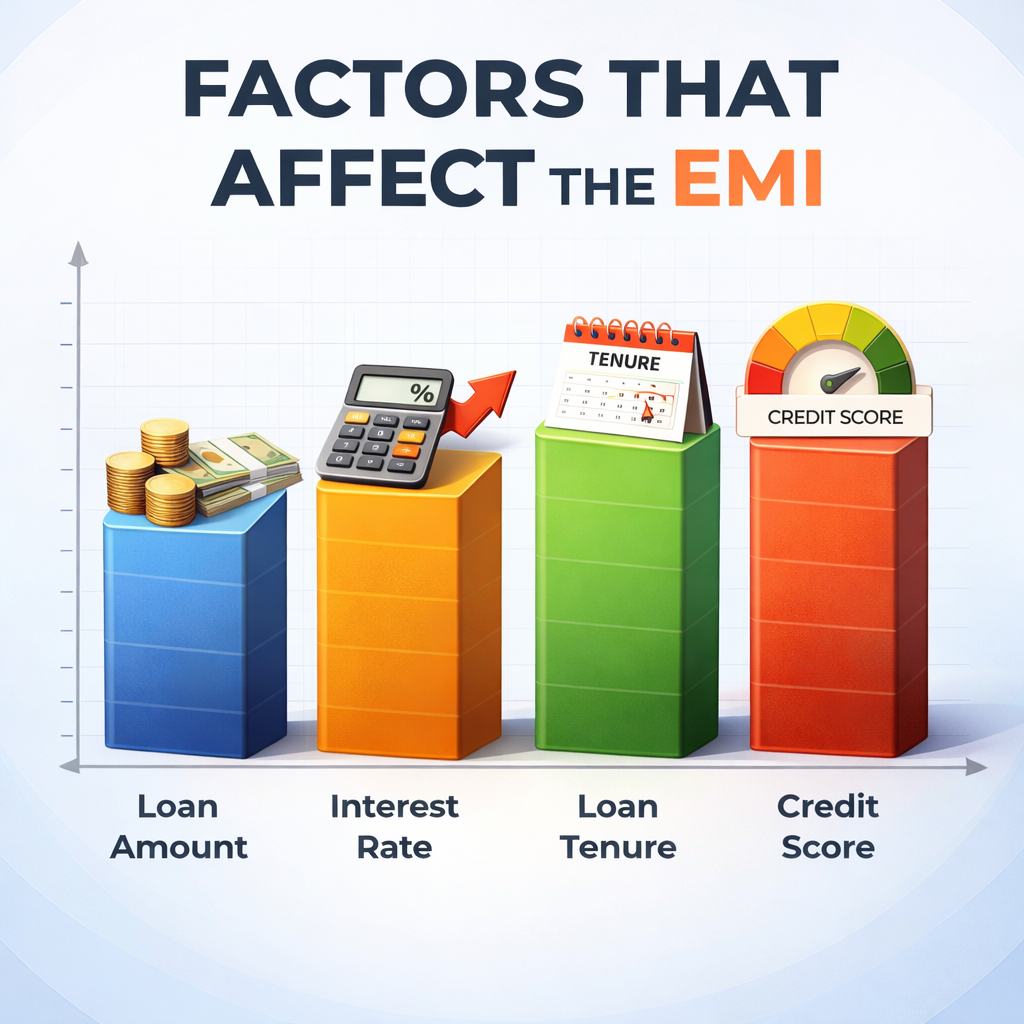

EMI is calculated using the reducing balance method with the formula: EMI = P × r × (1 + r)^n / ((1 + r)^n - 1), where P is the principal, r is the monthly interest rate and n is the tenure in months. The calculator on this page uses this exact formula.